Macro-Prudential Policy Framework

View more ![]()

State Bank of Pakistan (SBP) plays a pivotal role in ensuring stability of the financial sector. As a central bank, banking supervisor, and resolution authority, it has been entrusted with responsibilities to, inter alia, contribute to the stability of the financial system of Pakistan. A sound and stable financial system in turn is a key imperative for monetary and price stability, paving the way for inclusive and sustainable economic development. For this purpose, SBP has instituted both micro-prudential supervision tools (focusing on the soundness of individual institutions) and macro-prudential policy framework which aims to proactively assess and mitigate system-wide risks.

Financial Stability Department (FSD) of SBP is responsible for supporting the formulation and implementation of macro-prudential policy framework. It conducts comprehensive financial stability assessments, evaluates key systemic risks, and the resilience of regulated financial institutions to those risks. It also formulates corresponding policy recommendations. Coordinates the crisis preparedness function as well as various macro-prudential policy initiatives both within and outside SBP.

Financial stability reflects the state in which the financial system - financial intermediaries, financial markets, and financial market infrastructure - aids the smooth flow of funds between savers and investors in a structured and trustful manner. The financial sector is considered stable when financial institutions in general are:

The financial system’s stability is important to:

Given the importance of financial system in a well-functioning economy, ensuring the stability of the financial system has emerged as one of the key responsibilities of the central banks and regulatory authorities across the world. To achieve this goal, it is necessary for central banks to proactively identify and redress vulnerabilities which can build over time and across institutions, to preserve both soundness of financial institutions as well as public confidence and limit spillovers of risk and disruptions to other segments of the economy.

The preamble and Section 4B of the SBP Act explicitly delineate the stability of the financial system of Pakistan as one of the key objectives of SBP besides its primary objective of maintaining domestic price stability. Further, Section 4C(j) of the Act, among others, empowers SBP to use necessary macro-prudential tools for this purpose SBP has also developed a Macro-prudential Policy Framework. Furthermore, SBP Strategic Plan 2023-28 also emphasizes strengthening the financial stability framework as a key goal.

In order to ensure stability of the financial system, in general, and the banking sector in particular, an elaborate regime has been put in place at SBP, which comprises:

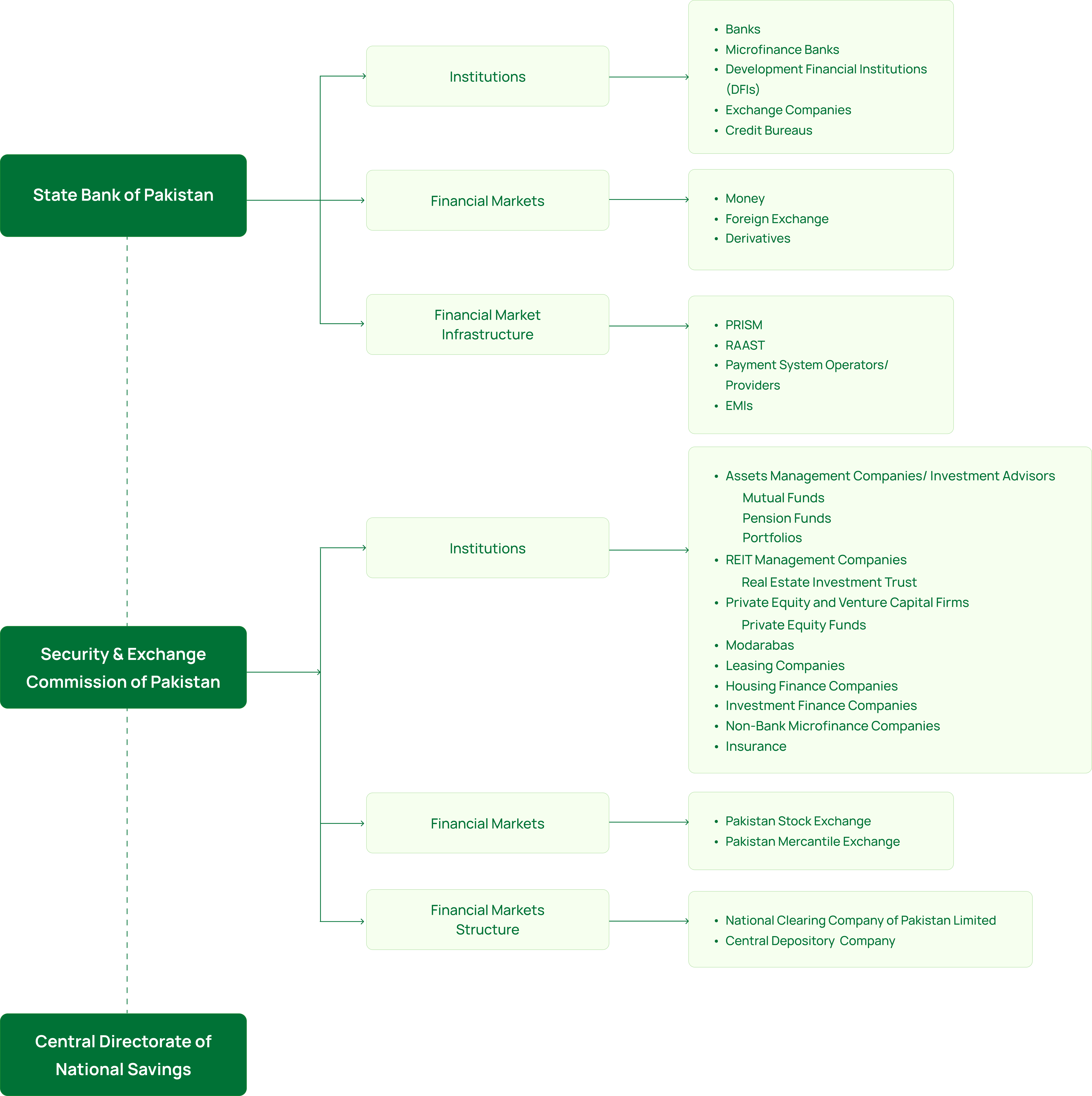

The financial sector of Pakistan mainly comprises banking institutions, development finance institutions (DFIs), microfinance banks (MFBs), non-banking finance institutions (NBFIs), insurance firms, financial markets, and financial market infrastructures. The supervision of financial institutions is entrusted with the SBP and the Securities and Exchange Commission of Pakistan (SECP). Detailed structure is given below.

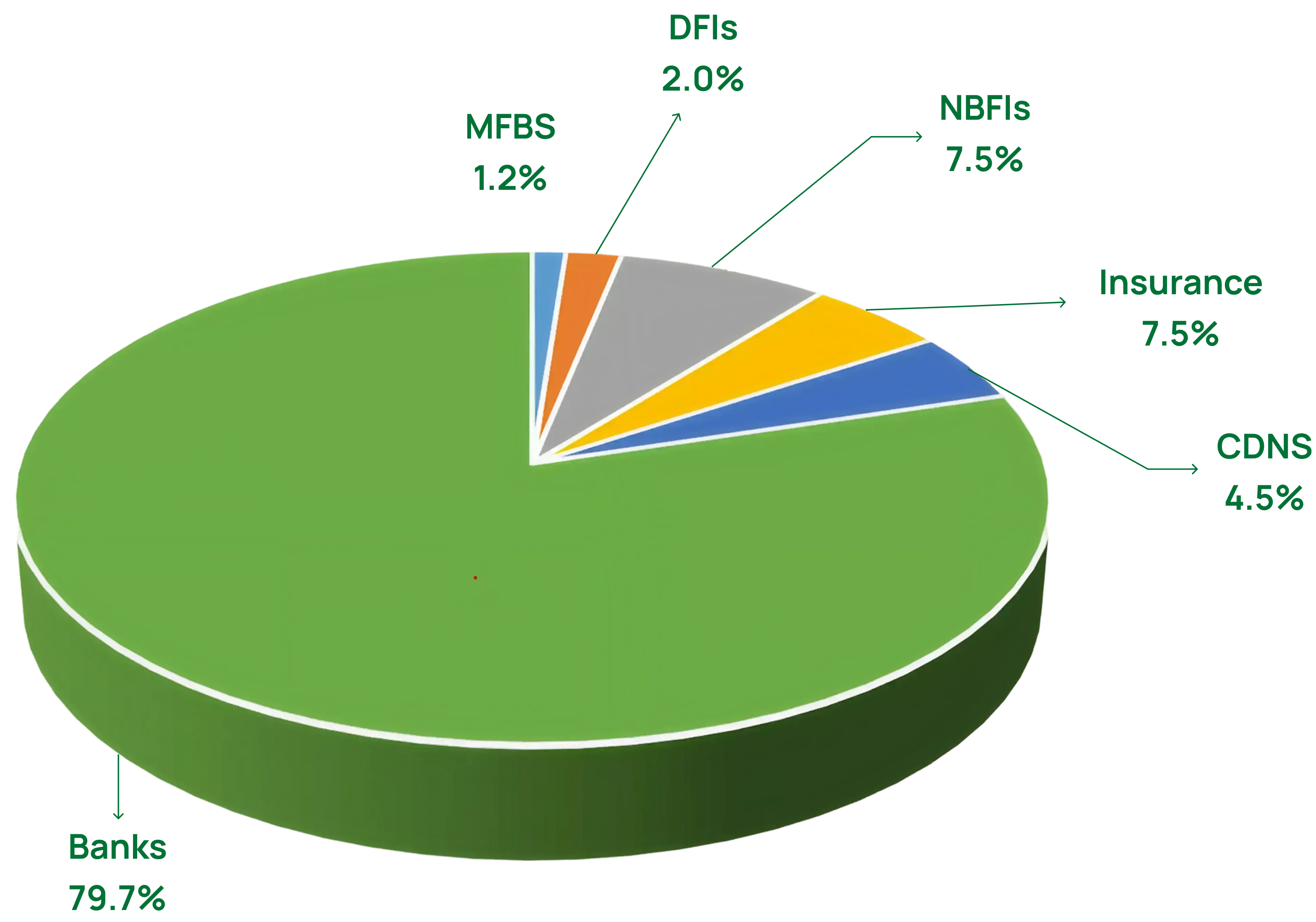

Pakistan’s financial sector is dominated by banks which contribute the largest part of the financial sector’s asset base and play a significant role in both intermediation process and payment system of the country. Therefore, the soundness of banking sector has a profound bearing on the overall financial and economic stability in the country.

Sources : SBP SECP and CDNS

SBP carries out regular assessments of systemic vulnerabilities and transmission channels of shocks to the financial sector and real economy. Besides informing the policy decisions, the assessments are also shared with market via different publications and data compendium as detailed below: